Chris Kerckhoff, AIF®, CFP®

In many areas of our lives, the importance of goal-setting seems obvious. If you go on a diet, you commit to losing a certain number of pounds. When you go on vacation, you plan where to go. These statements seem elementary.

When it comes to investing, however, the financial services industry would prefer you to start investing right away without ever setting a goal. That’s crazy.

Choosing an investment strategy without defining what you need the money for is like jumping on a plane without ever choosing a destination. Imagine booking a flight solely based on your tolerance for turbulence and your time horizon for the trip.

When it comes to flying, most people are only willing to accept the risk (speed, turbulence, etc.) and the travel time in cramped seats because they have a destination in mind.

Goal setting is a required starting point for successful investing.

The same is true for investing. Most people are only willing to take market risk and entrust their money to financial institutions because they want to achieve important milestones in their lives that require funds in the future.

Setting clear goals like retirement, funding college, or buying a home should play the primary role in recommending an appropriate allocation between safe, moderate and risky assets.

We never invest for clients without understanding their goals. Here’s how a goals-based approach helps you build the best investment plan possible, getting you in the right investment “vehicles” for your desired destination.

1. Your priorities define your goals.

A goals-based financial plan helps you plan for all your life goals, moving beyond the narrow thinking of a “retirement number” or “net worth target” to ensure you have the funds you need to live well today, while planning well for tomorrow.

When you create a few goals in BrightPlan, you’ll see all of them at a glance on the My Life Dashboard. The timeline view helps you easily check which goals are on track, at risk, or off track.

2. Your goals seem more achievable.

Whether you’re saving to buy a home, send a child to college or retire early, a savings plan helps you quantify what you’ll need. It also breaks down a larger savings target into achievable micro-goals. Breaking your monthly or annual savings across goals can help you prioritize which goals to save toward during a month when expenses run high.

3. It helps you save more—and understand why.

Saying, “I want to save 10% of my income this year” is not very inspiring. Try, “I need to save $175 per month for 18 months to take a dream trip to New Zealand.” That’ll get you somewhere.

Setting aside money for anything is tough, and that’s why it’s important to know why you’re saving. Goals-based financial planning takes advantage of a behavioral bias people have with money, called mental accounting. Mental accounting refers to our habit of earmarking money for certain goals, rather than (rationally) thinking that our money can be used for anything.

A goals-based financial plan helps you to take advantage of mental accounting to bucket your savings for important goals, which may motivate you spend less and save more.

4. You’re not just saving for a goal, you’re investing in it.

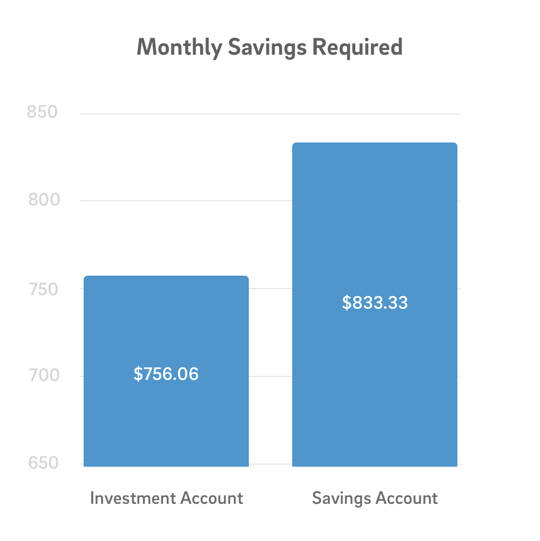

Compound returns can make a big difference in how much you need to save. Money put away for large, long-term goals should be invested. The returns can help your money not only beat inflation, but also grow in purchasing power over time. Compound interest can work in the short term, too—for example, if you plan to save $50,000 to buy a home in five years.

Look at the chart below to see how much you would need to save on a monthly basis in a savings account, vs. an investment account earning a 5% annual return.

5. You avoid over- or undershooting your target.

It may be hard to believe, but some people actually go overboard when saving for retirement. It can be because the goal is so far off, or because maxing out retirement accounts becomes a habit that is difficult to turn off.

One of the most liberating things we do for clients is help them discover what they’ll need for their long-term goals. That number gives them permission to strategically splurge—whether it’s on a family trip next summer, giving generously to a cause or upgrading the house.

6. Your risk is the right size.

A short-term goal, such as the vacation you want to take in three years, should have a low-volatility portfolio. A long-term goal like retirement needs a higher risk portfolio. BrightPlan can set up separate investment accounts for each of your goals, with an appropriate investment plan for each.

Funding both goals can help you weather the short-term swings in the riskier portion of your portfolio, because you know that the money you need soon is safe and readily accessible.

With a goals-based strategy, “risk of loss” becomes “risk of not reaching my goal.” That’s a critical shift in thinking when it comes to making decisions. For example, if you’ve set aside the money for a house five years down the road, then a 10% drop in the market is put into perspective.

You know that selling your investments won’t help you reach your goal, because that money has a job to do over the next five years until you need it. Instead of getting scared out of the market, knowing your goal may actually motivate you to invest a little more each month.

7. You can match your goals to the right types of accounts.

You don’t want to accidentally save your down payment for a home next year in your 401(k) or traditional IRA. Likewise, saving early in a tax-advantaged 529 for college can lead to more money to fund tuition. A goals-based financial plan gives you the strategy to choose the right accounts for your future.

Here are some examples of accounts we recommend for various goals:

- Retirement: Roth and Traditional IRAs, 401(k)s

- Education: 529s and Taxable Accounts

- Emergency Fund: High Yield Savings

- Buying a Home: High Yield Savings or Taxable Brokerage

- Leaving a Legacy: Trusts

When planning a trip, you get on the right plane to head to your destination. It should be the same with your investment philosophy. By taking a goals-based approach, you’ll improve your chances of arriving exactly where you’d like—whether it’s sending your kids to the college of their choice, setting up a charity, or finally taking that dream vacation.